The Fourth Bubble - Instability & The Problem Of Debt

Authored by Lance Roberts via RealInvestmentAdvice.com,

It didn’t take long. Over the last several years, we have discussed the risk of excessive monetary policy inflating a bubble in a variety of assets from debt, to real estate, to stocks. In March, it appeared as if the bubble had finally popped. However, the Fed’s quick response and massive monetary interventions ceased the asset bubble’s deflation and reinflated it.

Another Bubble

The idea of another bubble was put forth recently by Jeremy Grantham of GMO fame:

“At GMO, we dealt with three major events before this crisis, and rightly or wrongly, we felt ‘nearly certain’ that we would be right sooner or later. We exited Japan 100% in 1987 at 45x and watched it go to 65x (for a second, more significant than the U.S.) before a downward readjustment of 30 years and counting. In early 1998 we fought the Tech bubble from 21x (equal to the previous record high in 1929) to 35x before a 50% decline. Through 2007 we led our clients relatively painlessly through the housing bust.

In all three, we felt we were nearly sure to be right. Japan, the Tech bubbles, and 1929, which sadly I missed, were not new types of events. They were merely extreme cases akin to South Sea Bubble investor euphoria and madness. The 2008 event was also easier if you focused on the U.S. housing euphoria, a 3-sigma, 100-year event, or, simply, unique. We calculated that a return trip to the old price trend and a typical overrun in those extreme house prices would remove $10 trillion of perceived wealth from U.S. consumers and guarantee the worst recession for decades. All these events echoed historical precedents. And from these precedents, we drew confidence.

But this event is unlike all those. It is new, and there can be no near certainties, merely strong possibilities. Such is why Ben Inker, our Head of Asset Allocation, is nervous. and this is why you are worried or should be.”

Don’t Blame The Pandemic

While much of the media points to the pandemic as the “cause” of the economic problems, it isn’t.

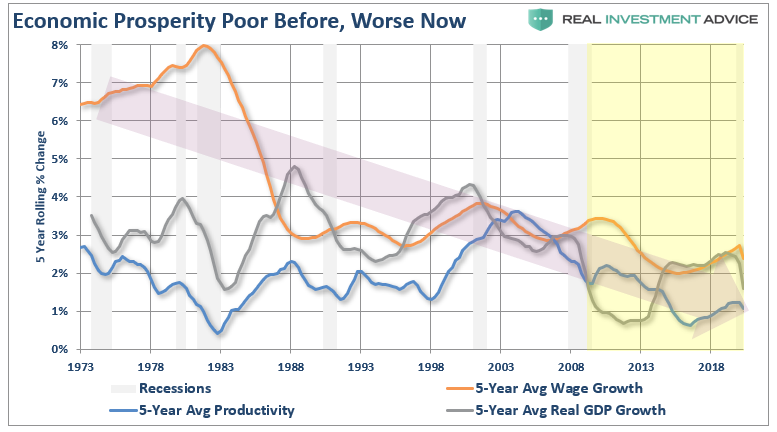

COVID-19 was merely the “pin the pricked the bubble.” If the pre-pandemic economy were as strong as previously reported, it would have weathered the blow better. However, the 5-year average growth of wages, productivity, and real economic growth tells the story.

Consequently, the surge in the stock market over the last decade gave an “illusion” of prosperity, that “prosperity” was relegated to a relatively small portion of the broader economy. As noted recently, the Fed’s policies are responsible for the “wealth gap.”

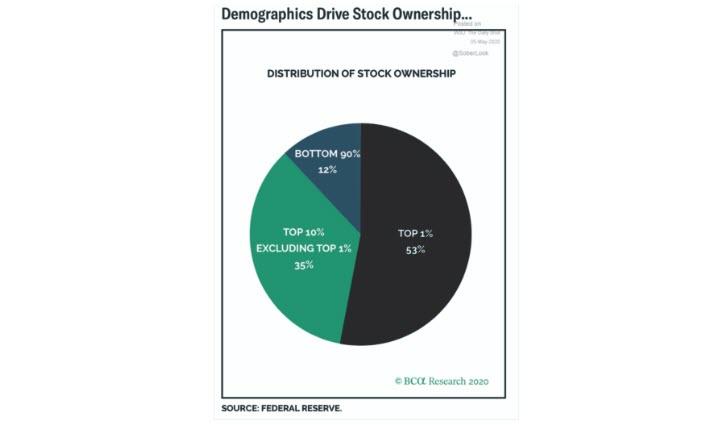

“This isn’t surprising. A recent research report by BCA confirms one of the causes of the rising wealth gap in the U.S. The top-10% of income earners own 88% of the stock market, while the bottom-90% owns just 12%.”

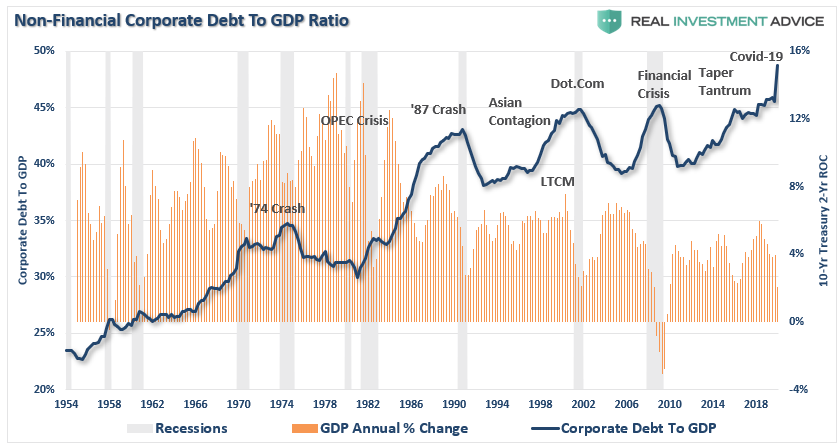

Reliance On Debt To Solve A Debt Problem

The reliance on debt, or what the Austrians refer to as a “credit induced boom,” has reached its inevitable conclusion. The unsustainable credit-sourced boom, which led to artificially stimulated borrowing, created diminished investment opportunities. Those diminished investment opportunities lead to widespread malinvestments, which we saw play out “real-time” in subprime mortgages in 2008 and excessive “share buybacks” over the last few years.

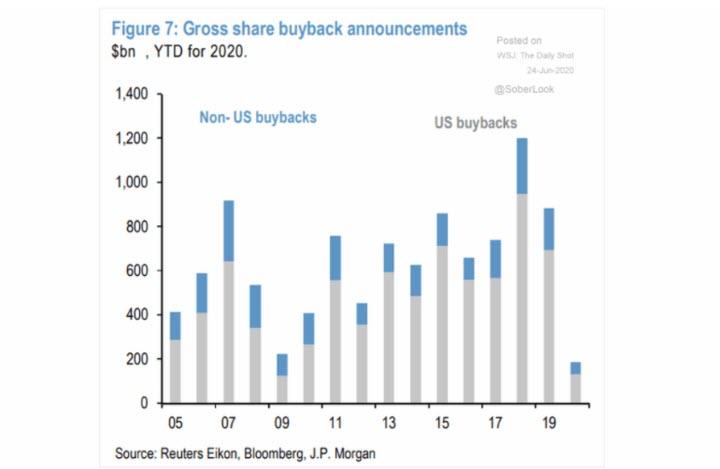

Now companies are struggling to take on more debt just to survive the economic downturn. Even as balance sheets are levering up, stock buybacks, a main support of the stock market over the last decade, are dropping sharply.

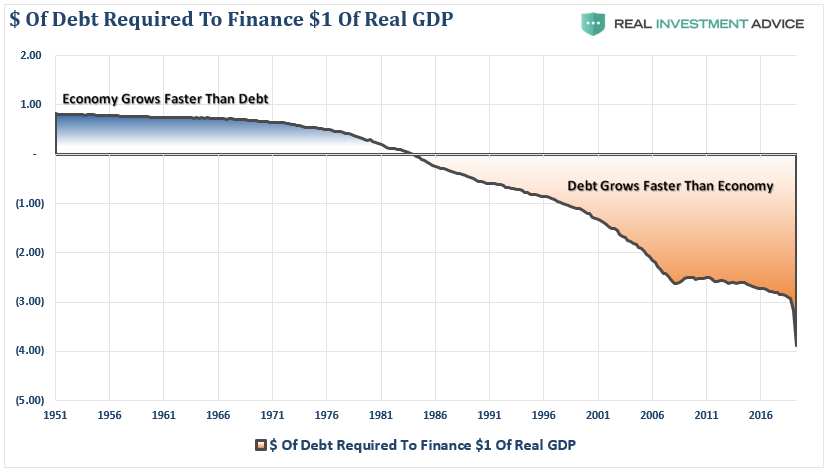

The Problem Of Debt

Unfortunately, given the Fed stopped the “debt reversion process” with the latest rounds of monetary interventions, nearly $4.00 of debt are required to create $1 of economic growth. This all but guarantees that future economic growth will be further retarded.

Such is a point made previously:

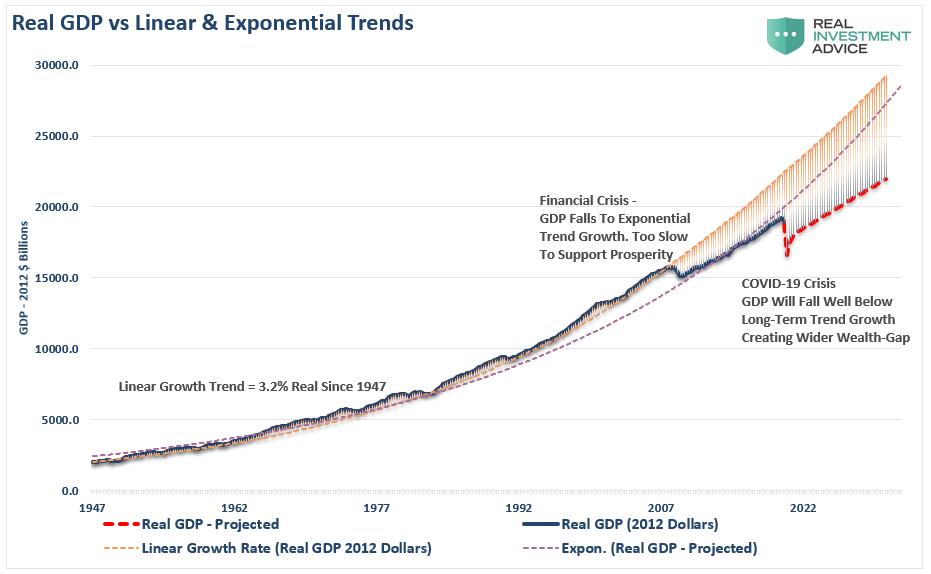

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.”

“The ‘COVID-19’ crisis led to a debt surge to new highs. Such will result in a retardation of economic growth to 1.5% or less. While the stock market may rise due to the Fed, only the 10% of the population owning 88% of the market will benefit. Going forward, the economic bifurcation will deepen to the point where 5% of the population owns virtually all of it.

That is not economic prosperity. It is a distortion of economics.

Bubbles, Bubbles, Bubbles

Jerome Powell clearly understands this risk. After a decade of monetary infusions and low interest rates, the Fed has created the largest asset bubble in history. However, trapped by their own policies, any reversal leads to almost immediate catastrophe as seen in 2018, and again in 2020.

“In the U.S., the Federal Reserve has been the catalyst behind every preceding financial event since they became ‘active,’ monetarily policy-wise, in the late 70’s.”

Not surprisingly, after the market correction in March, the immediate response stopped the correction from becoming a full-fledged bear market. However, this only forestalled the inevitable as we have seen a sharp rise in “speculative fervor” ever since. Investors, and the financial media, continue to assume there is investment risk due to the Fed. To quote Dr. Irving Fisher:

“Stocks have reached a permanently high plateau.”

Instability

It is imperative for the Fed that market participants, and consumers, “believe” in their actions. With the entirety of the financial ecosystem more heavily levered than ever, the “instability of stability” remains the most significant risk.

“The ‘stability/instability paradox’ assumes that all players are rational, and such rationality implies avoidance of complete destruction. In other words, all players will act rationally, and no one will push ‘the big red button.’”

The Fed had hoped they would have time, after a decade of the most unprecedented monetary policy program in U.S. history, to navigate the risks built up in the system. Unfortunately, they ran out of time, and the markets stopped “acting rationally.”

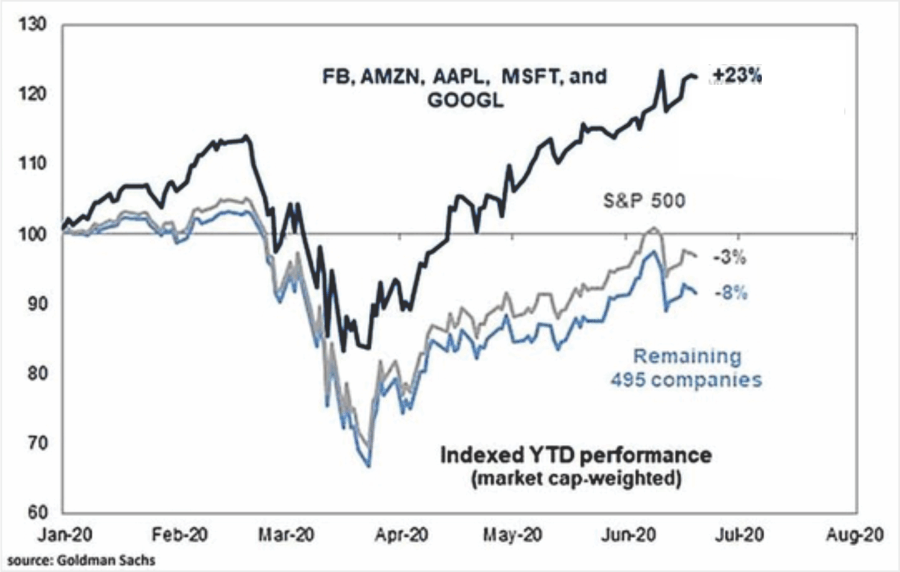

By not letting the system correct, letting weak fail, and allowing valuations to revert, the Fed has trapped itself into an even bigger bubble. One way to view this problem is by looking at the Nasdaq 100 versus the S&P 500 index. That ratio is now at the highest level ever.

Furthermore, that rise was not a function of a broad number of companies participating due to stronger economic growth and profits, but rather just 5-companies driving the surge.

If you don’t think this is important, I suggest you re-read Bob Farrell’s Rule #7:

“Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.”

Bubbles Aren’t About Price

“Market bubbles have NOTHING to do with valuations or fundamentals.”

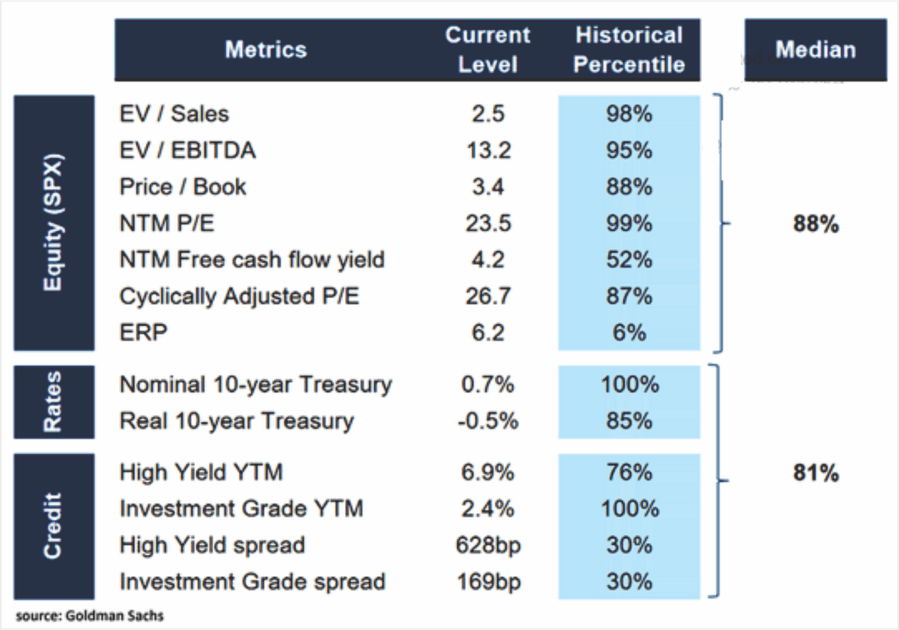

As we discussed last week, the market is now trading nearly 90% above multiple long-term valuation measures.

“One thing I had hoped for in 2018-2019 is a correction large enough to revert some of the excessive valuation levels which existed. Such would provide higher future returns over the next decade. Such would allow investors to reach their investment goals.

Instead, the Fed’s actions halted the correction. Subsequently, the ‘clearing process’ was not allowed to occur. The outcome has been increased levels of corporate leverage, and valuations remain grossly elevated on many different levels.”

Since stock market “bubbles” are a reflection of speculation, greed, emotional biases, valuations are only a reflection of those emotions.

It’s Elementary

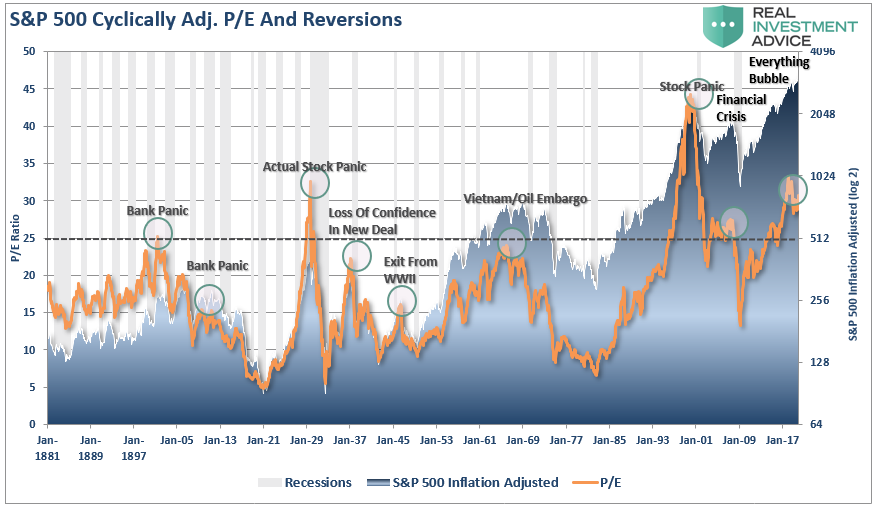

Bubbles can exist even at times when valuations and fundamentals might argue otherwise. Let’s look at an elementary example. The chart below is the long-term valuation of the S&P 500 going back to 1871.

Notice that except for 1929, 2000, and 2007, every other major market crash occurred with valuations at levels LOWER than they are currently.

Secondly, market crashes have been the result of things unrelated to valuation levels. Such as liquidity issues, government actions, monetary policy mistakes, recessions, and inflationary spike, or even a “pandemic.” Those events were the catalyst, or trigger, which started the “reversion in sentiment” by investors.

Market crashes are an “emotionally” driven imbalance in supply and demand. Such has nothing to do with fundamentals. It is strictly an emotional panic, which is ultimately reflected by a sharp devaluation in market fundamentals.

That is what started in March.

The Fed’s actions have only temporarily halted its inevitable completion.

The 4th-Bubble

“The current belief is the Fed will implement QE at the first hint of a more protracted downturn in the market. However, as suggested by the Fed, QE will likely only be employed when rate reductions aren’t enough.”

Credit markets’ implosion made rate reductions completely ineffective and has pushed the Fed into the most extreme monetary policy bailout in the history of the world.

So far, the Fed was able to inflate another asset bubble to restore consumer confidence and stabilize the credit market’s functioning. The problem is that since the Fed never unwound their previous policies, current policies are likely to have a more muted long-term effect.

However, with 50+ million unemployed, wage growth declining, bankruptcies on the rise, and banks tightening lending standards, the Fed’s attempt to inflate another bubble to offset the damage from the deflation of the last bubble, will work.

It has taken a massive amount of interventions by Central Banks to keep economies afloat globally over the last decade. There is little evidence that growth will recover following this crisis to the degree many anticipate.

Problems QE Can’t Fix

There are numerous problems which the Fed’s current policies can not fix:

-

A decline in savings rates

-

Aging demographics

-

Heavily indebted economy

-

Decline in exports

-

Slowing domestic economic growth rates.

-

Underemployed younger demographic.

-

Inelastic supply-demand curve

-

Weak industrial production

-

Dependence on productivity increases

The lynchpin in the U.S., remains demographics, and interest rates. As the aging population grows, they are becoming a net drag on “savings,” the dependency on the “social welfare net” will explode as employment and economic stability plummets, and the “pension problem” has yet to be realized.

While the current surge in QE has been successful in inflating another bubble, there is a limit to the ability to continue pulling forward future consumption to stimulate economic activity. There are only so many autos, houses, etc., that consumers can purchase within a given cycle.

Unfortunately, extremely high levels of unemployment, lack of incomes, and a slow economic recovery will likely undermine those hopes.

One thing is for certain. The Federal Reserve will never be able to raise rates or reduce monetary policy ever again.

The only question is, what will the Fed do if “all the king’s men can’t put Humpty Dumpty back together again?”

Comments

Post a Comment